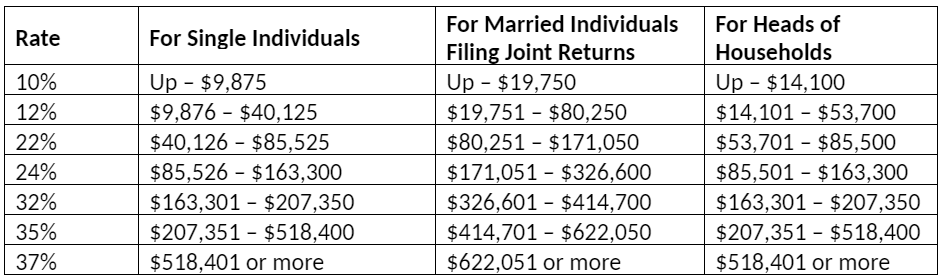

- Tax brackets and tax rates have changed. Every year, the tax brackets for taxable income are

adjusted based on the rate of inflation. Table 1 illustrates your marginal tax bracket based on

taxable income.

Table 1: Tax brackets for 2020

- The increased standard deduction has simplified filing for many. The standard deduction for married filing jointly rises to $24,800 for tax year 2020, up $400 from last year. For single taxpayers and married individuals filing separately, the standard deduction rises to $12,400, up $200 from 2019. For heads of households, the standard deduction will increase to $18,650, up $300.

- You may be eligible to take a $2,000 tax credit for each child. The credit is available to parents as long as your child is younger than 17 years of age on the last day of the tax year, generally Dec 31. It begins to phase out at $200,000 of modified adjusted gross income for single filers. The amount doubles to $400,000 for married couples filing jointly.

- Limitations on itemized deductions. If cash expenses that are eligible to be itemized fail to top the standard deduction, skip Schedule A and take the standard deduction. It’s that simple. If you itemize, please be aware that state and local income taxes, property taxes, and real estate taxes are capped at $10,000. Anything above cannot be written off against income. However, the IRS said it will grant a workaround for some taxpayers.Taxpayers that use pass-through entities (PTE), including S-corporations, some limited liability companies, and partnerships may qualify depending on your state. This workaround is not available for sole proprietors and single-member LLCs. According to the American Institute of CPAs, the PTE may deduct the entity’s state and local income taxes as a tax on the business at the federal level and avoid the $10,000 cap. State proposals would also provide that the owner may claim a credit on the owner’s state income tax return for the owner’s distributive share of the taxes paid by the PTE. It’s a complex maneuver that is only allowed by a few states, but it can help reduce your tax liability if you qualify.

For charitable contributions, you may generally deduct up to 50% of your adjusted gross income, but 20% and 30% limitations apply in some cases. In 2020, the IRS allows all taxpayers to deduct the total qualified unreimbursed medical care expenses for the year that exceeds 7.5% of their adjusted gross income.

- Penalties have been eliminated for not maintaining minimum essential health care coverage, according to the Tax Cuts and Jobs Act.

- Estates of decedents who die during 2020 have a basic exclusion amount of $11,580,000, up from $11,400,000 for estates of decedents who died in 2019. The annual exclusion for gifts is $15,000 for calendar year 2020, as it was in 2019.

- The maximum credit allowed for adoptions for tax year 2020 is the amount of qualified adoption expenses up to $14,300, up from $14,080 for 2019.

- Changes to the AMT–the alternative minimum tax. Tax reform failed to do away with the alternative minimum tax (AMT), but it snags far fewer people. The AMT exemption amount for tax year 2020 is $72,900 and begins to phase out at $518,400 ($113,400 for married couples filing jointly for whom the exemption begins to phase out at $1,036,800). The 2019 exemption amount was $71,700 and began to phase out at $510,300 ($111,700, for married couples filing jointly for whom the exemption began to phase out at $1,020,600). It’s confusing, but most tax software programs run both calculations for you.

- There is a 20% deduction for business owners. The new law gives “flow-through” business owners, such as sole proprietorships, LLCs, partnerships, and S-corps, a 20% deduction on income earned by the business. This is a very valuable benefit to business owners who aren’t classified as C-corps and can’t benefit from 2018’s reduction in the corporate tax rate to 21% from 35%. Individual taxpayers and some trusts and estates may be entitled to a deduction of up to 20% of their net qualified business income (QBI) from a trade or business, including income from a pass-through entity. In general, total taxable income in 2020 must be under $163,300 for single filers or $326,600 for joint filers to qualify. The deduction does not reduce earnings subject to the self-employment tax. There are limitations to the new deduction and some aspects are complex. Feel free to check with your tax advisor to see how you may qualify. Most tax software programs will run the calculation, too.

The points above are simply a summary. You may see provisions that will benefit you. You may also see potential pitfalls. If you have any questions or concerns, let’s have a conversation or you can consult with your accountant.